After a decade of success, have underwriting returns reached ‘what looks like a permanently high plateau’ of profitability?

Workers’ compensation insurers have enjoyed a decade of success.

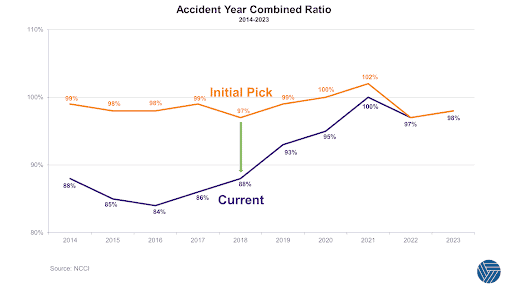

From an accident year perspective, initial combined ratio picks have turned out to have been conservative, resulting in significant reserve releases throughout the period.

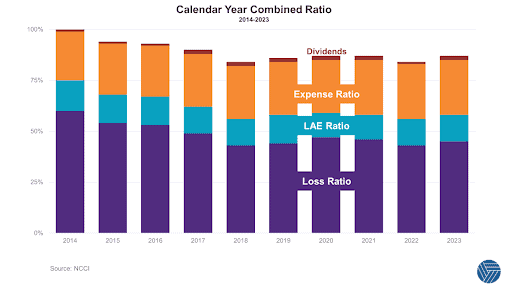

On a calendar year basis, the market has delivered combined ratios better than 100% every year since 2014 (having done so only once in the previous decade).

How has such profitability been possible, given increased competition in the market and the resultant broadening of terms and reduction of rates? The National Council on Compensation Insurance provides industry data and insights. They suggest that workers’ compensation insurance has entered a new era of low volatility with more consistent results and fewer of the steep peaks and troughs that have characterized previous market cycles.

We have identified four main drivers of recent profitability. Some do indeed reflect secular changes within workplaces, but we note with caution that others remain more cyclical in nature. In summary those drivers are:

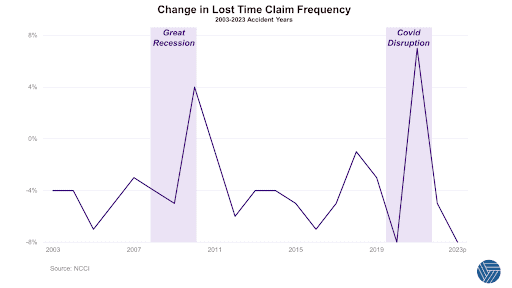

1. Changing Work Environment Improves Claim Frequency

Fundamental shifts have taken place in how Americans works. For office and healthcare workers that has meant more remote/hybrid work and fewer commutes. Factory workers have seen significant investments in and focus on workplace safety. Many of the most hazardous jobs have benefited from increased automation.

As a result the number of claims for lost worktime has declined in eighteen of the past twenty years and overall the number of claims declined by an annual average rate of 3.4% over the same twenty years.

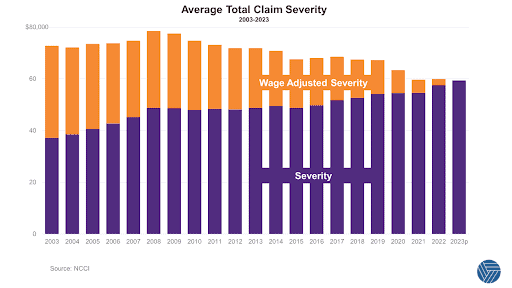

2. Wage Inflation & Lower Severity Trends

Although claim severity does increase due to higher wages and medical costs, those higher wages also increase the premium base. Adjusted for higher payrolls, claim severity peaked in 2008 at $78,500 (2023’s figure is $59,400). The average wage-adjusted claim severity has dropped 1% annually over the past twenty years.

The lower severity trends are the result of several favorable market developments:

- Medical & indemnity costs have become more consistent with the introduction of fee schedules and schedules of loss

- There has been downward pressure on prescription costs, and fewer opioids have been prescribed, lowering overall medical costs and increasing case closure rates

- Claims practices have improved

- Claims teams have become better at identifying large losses at early stages, possibly leading to more favorable outcomes

- A higher percentage of claims are now being settled, meaning claims teams have been able to limit loss development

However welcome these developments have been, we note that not all of these conditions are permanent. For example, there are fewer independent doctors in the U.S. as medical groups continue to expand, and such groups have more negotiating power when it comes to fee schedules, hindering carriers’ ability to limit adverse medical claims.

More importantly, the downward wage-adjusted severity trend is dependent on wage inflation continuing to outpace medical inflation. Any economic downturn would likely reverse that positive direction – the rise in severity in 2008-2009 coincides with the Great Recession.

3. Benign Economic Conditions Have Kept Claims Down

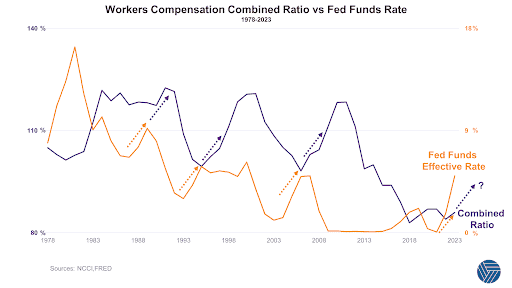

The other economic factor involves interest rates. For most of the past decade, low interest rates have promoted economic growth and workforce expansion. Since employers pay insurers premiums that are a percentage of payroll, expanding workforces and wages generates expanding premiums.

However, higher interest rates encourage competition among insurers and many new entrants have been tempted to enter the market to chase higher investment yield when interest rates swell. These cash flow underwriting practices inevitably soften the market, causing losses to rise. It is an observable trend that workers’ compensation combined ratios tend to spike two to three years after rate hikes: