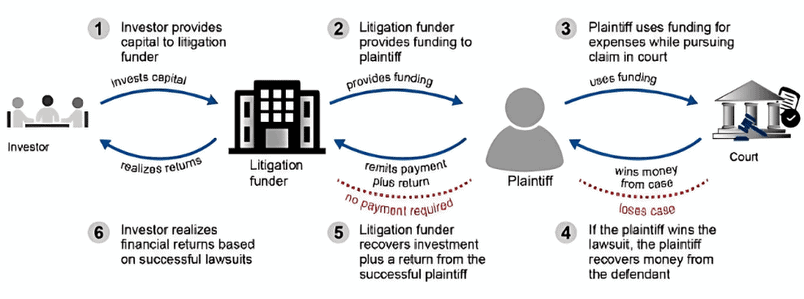

Introduction

Not every potential plaintiff can afford to fund their living expenses through the life of their claim, and not every attorney can afford to meet payroll while litigation is ongoing. Plaintiffs shouldn’t have to settle for low-ball amounts or 3rd rate attorneys.

Enter the third-party funder, willing to provide the working capital needed in return for a share of future recoveries.

Consumer funding for living expenses during a personal injury case usually involves a loan of up to 10% of the estimated claim value. If the plaintiff loses, the loan is forgiven. If the plaintiff wins, they pay back the original amount and a return, which can be an interest rate, a multiple of the original advance or a pre-negotiated share of the recovery.

Commercial funding (for corporate plaintiffs and/or their attorneys in commercial actions) may involve loans in the millions of dollars, and agreements may involve a single case, or a portfolio arrangement, where a law firm or business obtains funding in exchange for a share of the value of several cases. Funds can be used for any costs during litigation. Law firm funding demand is being driven by rising advertising costs, increased investments in data and analytics, and more mock trials.

Source: U.S. Government Accountability Office

Litigation funders include specialist legal claim companies who source capital from endowments and pension funds, traditional multi strategy hedge funds (with dedicated litigation finance desks), and high net worth individuals, family offices and hedge funds (without dedicated litigation finance desks).

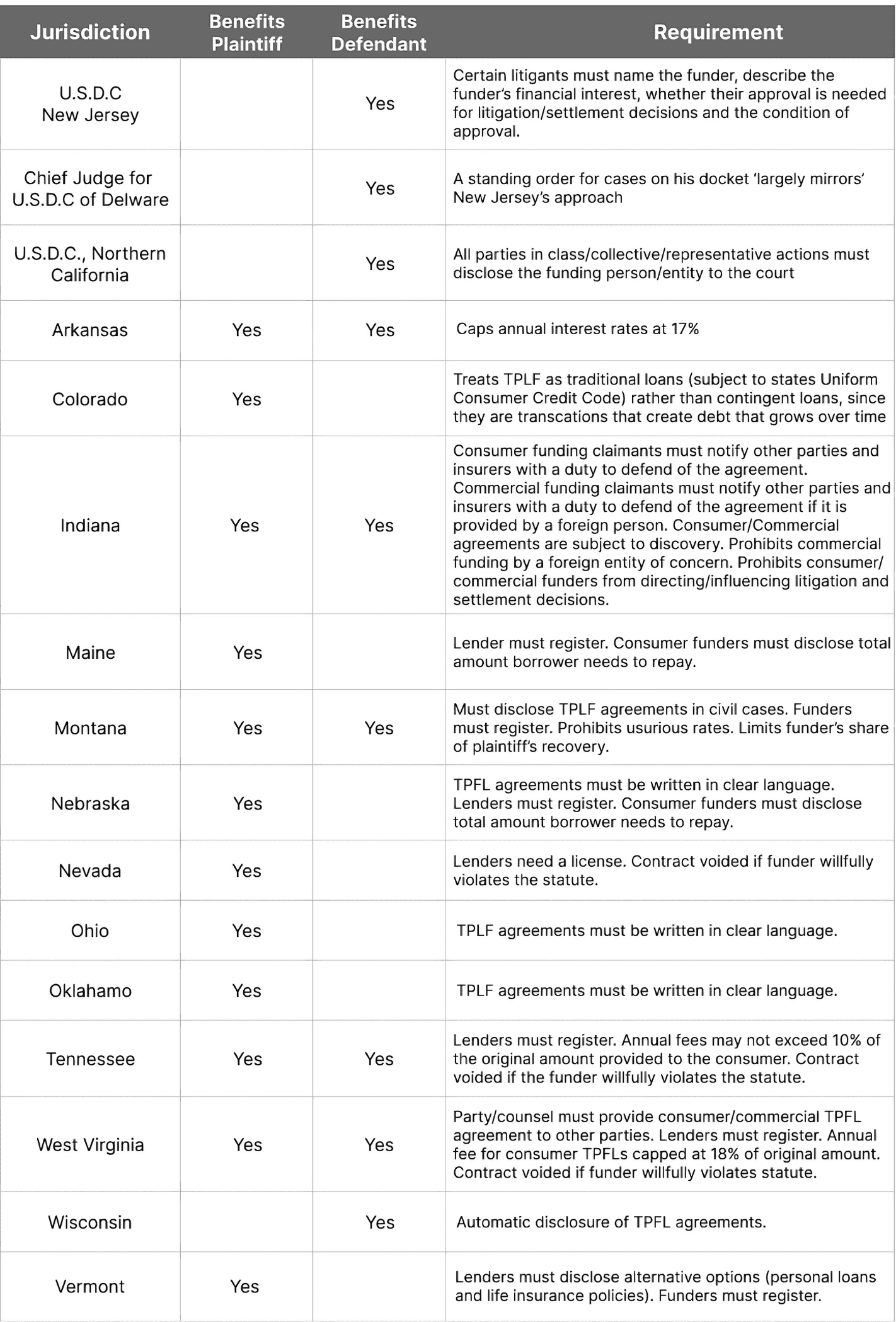

Disclosure

Plaintiffs and funders prefer to keep quiet about TPLFs. Some jurisdictions are taking steps to improve transparency and apply consumer protections:

For cases involving TPLF agreements, consider the following steps:

1. Educate the court on why disclosure is material (to facilitate settlements and allow defendants to see who controls the litigation/settlement discussions). TPLF agreements should be discoverable, because it gives funder’s a financial interest that accrues over time.

2. Argue that in New York TPLF agreements executed after liability is established are loans subject to NY’s usury statutes.

3. Seek to compel funders to appear for court-ordered settlement conferences, to enable direct negotiations and to change the optics (true adversary is a hedge fund/sovereign wealth fund).